This is the text of the Heuss Lecture (with audio of the Q & A below), delivered as part of the General Seminar series in the Wolff Conference Room of The New School for Social Research at 6 E. 16th. St. in New York on December 11, 2013.

From the 1970s on public debt increased more or less steadily in most, if not all, OECD countries, as it never had in peacetime. The rapid rise in public indebtedness was a general, not a national phenomenon, although in some countries, especially ones with low levels of inflation like West Germany, it began earlier than in others (Streeck 2011). In this essay I will emphasize the cross-national commonalities rather than the national specifics of the transformation of the “tax state” (Schumpeter 1991 [1918]) into a debt state and from there, at present, a consolidation state.[1] My argument focuses on the family of countries that adopted a regime of democratic capitalism, or capitalist democracy, after the Second World War, combining institutionalized mass participation in government with capitalist property relations and a market economy. By placing the current fiscal crisis of democratic-capitalist political economies in a historical context — in other words, treating it as a step in a historical sequence, not as a single event — I hope to shed light on the underlying dynamics of the crisis, beyond what static-technical theories of public finance have to offer.

The context within which I will situate the fiscal crisis of contemporary democratic states I conceive as a process of capitalist development. By this I mean the historical trajectory that led to the neoliberal revolution after the 1970s and abolished the “mixed economies” (Shonfield 1965; Shonfield and Shonfield 1984) of the three postwar decades, resulting in a more or less continuously growing role of markets including international markets in political-economic governance. In line with Schumpeter’s early research program of “fiscal sociology” (Schumpeter 1991 [1918]), I discuss public finance as both an indicator of and a causal factor in an evolving relationship between political rule and the economy, or more precisely, between the democratic state and modern capitalism.[2] Approaching the politics of public debt in this way, I will show that political-economic theories in the tradition of Public Choice, which attribute the rise in government debt to an inherent tendency of democracies to “live beyond their means”, cannot account for the fiscal crisis of today. After rejecting what I call the democratic failure theory, and based on the record of the last four decades, I will present a list of proximate causes accounting for the rise in state indebtedness and relate them to what I consider, for the purposes of my narrative, the ultimate cause behind them. That cause, I will argue, is the long-term decline in the growth performance of advanced capitalist economies and their subsequent inability to honor the promises of economic and human progress on which their legitimacy depended and depends.[3]

Following my analysis of the genealogy of the current crisis of public finance, I will turn to the five years that have passed since the near-crash of the global financial system in 2008, to outline what I perceive to be a new politics of debt management by consolidation. As I will argue, this includes a profound restructuring of the democratic-capitalist political economy in continuation of the neoliberal transformation of the last two decades of the twentieth century, in the direction of a state that is “leaner,” less interventionist, and, in particular, less receptive to popular demands for redistribution than was the case for states of the postwar period.[4] Special attention will be paid to the relationship between the politics of government debt on the one hand and social and economic inequality on the other.

Democratic Failure?

Democratic capitalism is a historically recent phenomenon. It became firmly institutionalized as a political regime only after 1945 under the international hegemony of the New Deal United States and, at least in Europe, built on social-democratic traditions (for many others Ruggie 1982; Judt 2005; Reich 2007; Judt 2009). In democratic capitalism, governments are expected to intervene in markets to secure social justice and stability as defined and demanded by a voting majority. This is because without political correction of a Keynesian and Beveridgean kind, free markets tend to give rise to cumulative advantage, also known as the “Matthew effect” (Merton 1968), which would make them unpalatable to a democratically empowered citizenry.[5]

Average public indebtedness among OECD countries more than doubled in the roughly four decades between the 1970s and 2010 from about 40 percent of GDP to more than 90 percent (for a sample of twelve major OECD countries, see Figure 1). As pointed out, increasing public debt was a general phenomenon in almost all countries of democratic capitalism. Differences between countries did exist, but in a longitudinal perspective, they reduce mostly to time lags and appear of minor significance in light of the universal nature of the process. Note that the rise of indebtedness was halted in the mid-1990s for about a decade, to resume only in 2008, the first year of an apparently never-ending financial crisis when state indebtedness started its steepest incline of the period under observation. I will return to this later.

Economic-institutionalist theories in the tradition of writers like James Buchanan attribute the increase in public debt since the 1970s to an inherent tendency of political democracy to overspend, caused by short-sightedness of voters and opportunism of politicians (Buchanan 1958; Buchanan and Tullock 1962; 1977; Buchanan and Wagner 1977). Where Public Choice transmutes into a theory of democratic failure, the claim is that public deficits and public debt are due to majoritarian electoral pressure from below for redistribution through public spending. In the following I will argue that this account, based on highly stylized hypothetical assumptions on “rational” behavior under democratic conditions, appears highly implausible when the increase in public debt is placed in the context of other events and developments that happened in the OECD world during the same period. This is because the growth of public debt was accompanied by a steady decline in both democratic mobilization and the distributional position of mass publics, pointing to a secular contraction of the power resources and redistributive capacities of the very democratic politics that are held responsible by theories of “public choice” for the rise in public indebtedness since the 1970s.

As to democratic power resources, participation in national elections in the OECD world peaked in the 1960s when it was as high as 84 percent on average for 22 countries (Figure 2). From there it dropped continuously from decade to decade and reached 73 percent in the eleven years from 2000 to 2011 (Schäfer and Streeck 2013). Unionization attained its highest postwar level in the 1970s and then began to fall everywhere (for six major countries, see Figure 3).[6] A third form of mass political participation, “industrial action”, also known as strikes, practically ended in the 1980s (see Figure 4, which omits Italy where strikes were extremely frequent in the 1970s but ceased almost entirely in the 1980s).

The decay of popular participation in redistributive politics was associated with a continuous loss in the distributional position of popular majorities. Unemployment increased everywhere as governments withdrew from the postwar promise of politically guaranteed full employment. Today, unemployment rates between five and ten percent are considered normal in capitalist democracies (Figure 5), de-unionization and often painful “reforms” of social security systems notwithstanding.[7] Even Sweden, the classical country of full employment labor market policy, has since the end of the 1990s been content with a “natural” level of unemployment hovering between six and nine percent (Mehrtens 2013). In parallel, income inequality has steadily increased in most countries until the middle of the first decade of the 2000s (Figure 6). One factor behind this was a massive decline of the wage share almost everywhere (Duménil and Lévy 2004; Kristal 2010; Ryner 2012) caused by a lasting decoupling of wage increases from increases in productivity. This was, not surprisingly, most pronounced in the United States, where by the end of the 1970s average hourly earnings ceased to follow productivity, embarking on a long stagnation while productivity continued to go up. Increases in household incomes during the period in question were solely due to higher participation of women in the labor market (Kochan 2013, Figure 7).[8]

Summing up, the rise of public debt — the arrival of the debt state — took place alongside a neoliberal revolution in the postwar political economy. At a time when democratic-redistributive intervention in capitalist markets became ineffectual on many fronts, increasing public debt is unlikely to be explained by excessive democratic power on the part of voters and workers. In fact, rather than electorates extracting unearned incomes from the economy, growing government indebtedness in OECD nations was accompanied by a lasting decline in in the distributional position of popular majorities, which in turn was associated with a secular decay of the power resources (Korpi 1983) of redistributive democracy.

Proximate Causes, Ultimate Cause

To account for the increase in government debt across a wide range of countries over an extended period of time, it seems useful to draw on the proven distinction between proximate and ultimate causes (Thierry 2005). The parallel build-up of debt in capitalist democracies was produced by a variety of specific factors that, while often interrelated, differed between countries and over time. All of these proximate causes, however, point back to one common, ultimate cause: a secular decline in economic growth in the democratic-capitalist OECD world. Seen from this perspective, the accumulation of public debt since the 1970s appears as part of a variegated response of countries and actors to declining growth and to the pressures on the politics of rich capitalist democracies that resulted and result from it.

The following, incomplete list includes some of the most important proximate causes of the rise of public debt during the period in question.

1. Public debt began to increase in the mid-1970s, and in particular in the early 1980s as a result of an OECD-wide recession which activated automatic fiscal stabilizers and, in some countries, called forth “Keynesian” stimulus spending. The “Second Oil Crisis” in 1979 caused higher expenses on unemployment benefit and active labor market policy while lowering public revenues, especially from payroll taxes. The same was true for the contraction of employment following the deflationary monetarist policy of the U.S. central bank under Volcker after 1979, with interest rates at times exceeding 20 percent, and the British turn to monetarism under Margaret Thatcher. Generally, the revocation of the postwar commitment to politically guaranteed full employment — a commitment that had begun to cause high and rising inflation at the end of postwar growth — and the acceptance on the part of governments of a residual level of unemployment as a natural condition was bound to put pressure on public finance as long as retrenchment of the postwar welfare state had not yet been accomplished.

2. The end of both growth and inflation led to a sharp increase in tax resistance, first in the United States and then elsewhere in the OECD world. In response, several countries passed tax reforms to eliminate what is called “bracket creep”: the movement of tax payers into higher income tax rates with rising nominal incomes. In subsequent years, “globalization” and the resulting international tax competition (Genschel and Schwarz 2013) motivated tax cuts for high income earners and corporations.[9] Emblematic for this was the tax reform during Ronald Reagan’s first period of office (1981-1985), which together with deflation and an unprecedented arms build-up was instrumental in causing the most dramatic rise in government debt since the Second World War (Greider 1981; Stockman 1986). While tax revenue had until the mid-1970s by and large kept pace with public spending, by the late 1980s it began to stagnate until it started declining after the end of the century (Figures 8 and 9). By 2010, taxation levels were back where they had been two decades earlier.

3. The 1990s were a time when OECD nations managed to bring down public spending in an effort to match it to stagnant and indeed declining tax revenue (as seen in Figure 8). In part, this was made easier by the end of the Communist bloc and the “peace dividend” it wrought. But it was also due to deep reforms of welfare state institutions. It seems reasonable to consider welfare state reform as a time-lagged response to the rise in social spending after the end of politically guaranteed unemployment. Retrenchment of social protection was championed in particular by the Clinton administration which, following its defeat in the mid-term elections of 1994, vowed to “end welfare as we know it.” In Germany, welfare reform was delayed by unification as the West-German social policy regime was translated one-to-one to the Neue Länder (Streeck and Trampusch 2006). A decade later, however, the social-democratic Schröder government passed the so-called Hartz IV legislation. Depending on the country, welfare state reform did not always and necessarily result in lower aggregate spending, at least not immediately; it did, however, cut individual entitlements in reaction to rising numbers of long-term unemployed and other recipients of social assistance. The 1990s, which may be described as a first period of fiscal consolidation, show that mass democracies, if placed under enough economic pressure and with voters sufficiently demobilized, are quite capable of curtailing social protection and generally imposing economic hardship on a majority of voters in the interest of “sound finance.”

4. By the late 1990s, a country like the United States had achieved a budget surplus (Pierson 1998; 2001). This did not last long, however, as it was soon to be wiped out after 2001by deep tax cuts combined with a steep increase in military spending, very much on the model of the first Reagan administration. Given that the “Bush tax cuts,” as they came to be called, overwhelmingly benefited corporations and the very rich (Hacker and Pierson 2011), they cannot possibly be attributed to an excess of redistributive democracy.[10] Quite to the contrary, the restored public deficit was used as an argument for further cuts in public expenditure, as military spending was untouchable and higher taxes on high incomes politically infeasible. Current debates on balancing the U.S. federal budget continue to focus almost exclusively on the so-called “entitlements,” in particular to social security and health care. Generating a public deficit by simultaneously cutting taxes and raising military spending corresponds to the strategic concept of the ultra-liberal American Right as organized by the anti-tax activist Grover Norquist. The strategy is summed up in the slogan, “starving the beast,” the beast being the residual welfare state of the post-New Deal United States.[11]

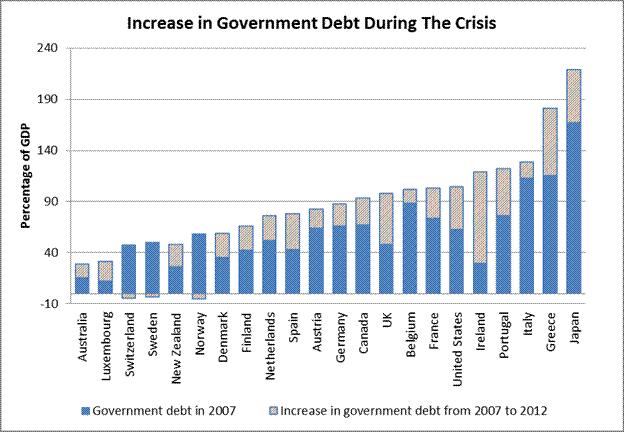

5. The financial crisis of 2008 caused the greatest hike in public indebtedness ever, due to the immense costs of both the rescue of the financial system and the stimulus spending required for keeping national economies from collapsing (for a selection of countries see Figure 10). Like tax cuts for the rich, “Star Wars” and the invasions of Afghanistan and Iraq, the absorption after 2008 of unsustainable private debt by the state as a debtor of last resort after 2008 cannot be attributed to irresponsible greed among voters and politicians. The emergency measures taken in 2008 wiped out all of the – politically very costly – accomplishments of the consolidation efforts of the 1990s and restored the level of public debt to the trend line for the forty-year period beginning in the mid-1970s. Contrary to public choice theory, the most dramatic leap in public indebtedness since the 1970s was a case of failure, not of democracy but of capitalism, in particular in its new form of financial capitalism.

How are the various proximate causes of the fiscal crisis of rich democracies related? The common ultimate cause, I suggest, behind the proximate causes effective along the trajectory of the public debt build-up was the declining growth performance of the OECD world (Figure 11). After 1974, average real growth per year in OECD countries over five year periods fluctuated between two and three percent, apart from two peaks at the end of the 1980s and the 1990s when it rose to between three and four percent, albeit only for a short time. Thereafter, in the one-and-a-half decades since 1998, i.e., ten years before the Great Recession, average growth rates declined almost steadily until they bottomed out at zero in 2010. In addition, with the end of inflation in the 1980s the automatic devaluation of public debt ended as well. Moreover, low growth during the same period resulted in average unemployment rates between six and seven percent. After 1998 it also kept debt ratios high although budget deficits almost disappeared in 2002-2008 due to consolidation efforts. They were, of course, to come back with a vengeance as a result of the financial crisis.

Pulling together ultimate cause and proximate causes, weak economic growth-induced governments and central banks in the 1970s — with the exception of the Bundes bank after 1974 — to accommodate wage pressures in order to preserve employment, which resulted in inflation. Monetary stabilization in the 1980sto end stagflation produced unemployment and thereby upset the fiscal balance of social security systems; it also added to tax resistance, which was facilitated by “globalization” enabling mobile assets to migrate between jurisdictions. Globalization also called forth “supply-side policies” including tax relief for corporations and the rich. It furthermore inspired financial deregulation, or “financialization” (Krippner 2011), in an attempt to restart the capitalist profit engine, especially in Anglo-American countries. As we know now, this did not really work and growth rates under financialization continued to decline. In the end, when the strategy collapsed in the Great Recession[12], it turned out to have produced pseudo-growth at best.

Over time, insufficient growth gave rise to a sequence of different crisis configurations, with (I) high inflation and low debt in the 1970s followed, from 1980 to 1993, by (II) low inflation and public and private debt rising simultaneously, and from 1994 to 2007 by (III) low inflation, receding public debt, and further increasing private debt. Since 2008, we continue to see (IV)low inflation, now combined with slightly declining private debt and further increasing public debt (Figure 12 for the U.S.; the pattern for other countries is essentially the same, with variations reflecting contingent national circumstances). Overall, the increase in public debt was part of a general rise of indebtedness in capitalist countries, which coincided with low growth. Thus the aggregate debt burden of the United States, comprising the debt of government, households, and non-financial as well as financial corporations, doubled in four decades from four-and-a-half to nine times the country’s GDP (Figure 13), of which government debt accounted for only a small share. The fact that the rise in government debt since the 1980s was embedded in a simultaneous rise in aggregate debt [13] tends to be overlooked in public discourse, in particular where fiscal problems are attributed to a failure of democracy. Growing overall indebtedness — the accelerating investment of savings and freely created fiat money in promises of future repayment effectively conditional on economic growth — would appear to be an insufficiently understood aspect of contemporary capitalist development.

Re-Building Confidence

The crisis of 2008marked the beginning of a new era in the politics of public debt, and generally in the relationship between global capitalism and the state system. As states accepted vastly increased indebtedness in order to rescue their national economies from the fallout of the collapse of the financial industry, investors in public debt became doubtful whether governments would ever be able to honor their unprecedented financial obligations, and whether public debt might have reached a point where states would find it more in their interest to default than to pay up. Declining investor confidence found expression, among other things, in a flurry of changing judgments on national public finances, meted out by the three U.S. rating agencies and in rising and fluctuating risk premiums on government bonds. Not surprisingly, economists went to work to calculate the debt level beyond which a country would cease to be solvent because its debt would render its economy unable to grow (Reinhart and Rogoff 2010). [14]

It soon turned out, however, that the matter was more complicated. Apparently, if there was a critical threshold, it was different for different countries. The United States continued to be charged a risk premium close to what “the markets” require from Germany, even though its government has long refused to address the country’s decades-old “double deficit.” Rather than specific numbers, discussions began to focus on intangibles like the trustworthiness of a country’s politics and the confidence it inspired in the psychology of owners of financial assets. In a more technical language, what was looked for was credible commitments on the part of countries to servicing their debt, come what may. I suggest that it is in this context that the rise of austerity as a political imperative for — some — debtor countries must be seen.

The politics of public debt may be conceived in terms of a distributional conflict between creditors and citizens (Streeck 2013, 117-132). Both have claims on public funds, the ones in the form of commercial contracts and the others of rights of citizenship. In a democracy, citizens may elect a government responsive to them but “irresponsible” from the viewpoint of financial markets, one that in the extreme case expropriates its creditors by annulling its debt. As accumulated debt grows and investors must be more cautious as to where they put their money, creditors will seek guarantees that this will not happen to them –that their claims will always be given priority over those of citizens, for example of pensioners demanding the pension that state and employers promised to them when they were workers.

“Structural reform” of domestic spending to cut the “entitlements” of the citizenry is one important way of reassuring creditors that their money will be safe.[15] Another is institutional change, such as balanced budget amendments to national constitutions, or international obligations to honor commercial before political debt. I consider extracting credible commitments of this kind — where there is broad space for creativity with respect to their concrete form[16] — as the driving force of the transformation of the debt state of the last third of the twentieth century into what I call the consolidation state of the future.

Looking at Europe[17], what is peculiar here is that what is to be the restoration of investor confidence takes place not just in national but also in international politics through a deep restructuring of the European state system, as demanded by both the European Union and, in particular, European Monetary Union. To reassure creditors, states agree to tight mutual surveillance, for example under the Fiscal Pact, tying each other’s hands to rule out default and constrain one another to get fit for debt service. This involves far-reaching sacrifices of national sovereignty in exchange for arrangements amounting de facto to a mutualization of public debt, to guarantee bond holders that they will be paid even if a member state was to become insolvent. Since debt mutualization cannot be popular with voters in countries that would have to pay for it, it is typically not done in the light of day but rather inside the entrails of the European Central Bank, whose President has famously vowed “to do whatever it takes to preserve the euro.”[18][19]

How much and what kind of “confidence” the “markets” must be provided with by debt states is far from understood. Clearly creditors will not complain if states fearing the fear of the markets do more than would in fact be necessary. Since international capital markets are not subject to competition law, it also cannot be precluded that institutional investors will collectively drive up the price of their trust. States, in turn, may use financial regulation to force certain categories of investors, like insurance companies, to buy and hold their bonds. The strategic games that are being played here will not end once the current crisis will be declared over, if it ever will. States will for a long time be dependent on financial markets, even with consolidated finances, if only for refinancing their remaining debt (which will be considerable for many years). In any case, financial markets may need government debt as a safe haven for investment. Bargaining over the rebuilding of the democratic state in the face of high debt, at the national as well as international level, will therefore not cease, with citizens trying to defend their social rights and creditors threatening higher risk premiums unless the primacy of their titles is firmly established in international treaties and national fiscal regimes and constitutions.

As is increasingly being noted, building investor confidence by way of imposing austerity on national economies may not in all circumstances achieve its objective. Austerity may impede economic growth by cutting demand, rather than promoting it by, among other things, creating “rational expectations” on the part of the “real economy” for low taxes and higher growth in the future. Apparently, as claimed by Blyth (2013) and others (Boyer 2012), expansionary austerity has never really worked in a financial crisis. While austerity may shift an increasing share of a society’s resources from citizens to creditors, it may shrink the sum total of available resources. Obviously the second effect could, in particular in the longer run, suppress the first effect as low growth might undo whatever confidence may have been gained through austerity.

Public Debt and Social Inequality

The build-up of public debt since the 1970s was in complex ways connected to the increase in economic inequality that occurred at the same time, and this holds true also for the current politics of consolidation. As growth rates declined and unemployment became endemic in the OECD world after the end of inflation, the wage and income spread increased, and so did public spending. Dwindling unionization and the “withering away of the strike” (Ross and Hartman 1960) contributed their share to rising income inequality (Western and Rosenfeld 2011). Tax collection became more difficult due to growing resistance, and later also because of international tax competition in an increasingly open global economy. Public revenues fell as a result, further adding to public deficits and public debt. Distributional gains on the part of capital and of segments of the middle classes, made possible by a growing low-wage sector and less progressive taxation, produced a savings overhang that was looking for safe investment opportunities. Tax reforms aimed at dissuading firms and high earners from exiting to less demanding jurisdictions reinforced this, expanding both the demand for and the supply of sovereign credit. In the 1990s at the latest, governments found it necessary to allow the financial industry to expand far beyond traditional limits, among other things by creating new credit instruments benefiting states increasingly dependent on borrowing at favorable rates. Financialization in itself added to income inequality, both between sectors and within (Palley 2008; Tomaskovic-Devey and Lin 2011).

States borrowing from their citizens instead of taxing them make another, independent contribution to economic and social inequality. Owners of financial assets who can lend to the state what it would otherwise confiscate earn interest on what remains their capital. They may also leave their wealth to their offspring, especially where inheritance taxes have been cut or abolished for fear of taxpayer exit. A complementary effect, incidentally, is at work under “privatized Keynesianism” where liberalized credit serves to replace social assistance or supplement low wage. The result is that the poor have to repay with interest what would have been their wage or social benefit with better employment, stronger trade unions, and more public intervention (Mertens 2013).

Moreover, as the debt state in its current form as consolidation state reassures its creditors that their claims to public funds will take precedence over the claims of citizens, it essentially expropriates social rights and politically created entitlements intended to protect social cohesion. Privatization of public services and a reduction of public social investment make for less egalitarian access to resources essential for equality of opportunity in an advanced “knowledge society.” As a result, social mobility for future generations is likely to diminish, as is already the case in the United States (Karabel 2012). With consolidation continuing, patterns of public spending will follow tax systems in becoming less progressive.

Concluding Remarks

What is coming? We have seen how the emerging consolidation state is cutting itself down, through public austerity and the progressive privatization of infrastructures and social services. The question is whether this will restore economic growth and democratic legitimacy to post-2008 capitalism. Seeking to achieve these goals as in the past two decades by relying on a lax monetary policy and a bloated financial sector apt any time to produce new bubbles may at a minimum be risky, and it could easily become self-destructive when another “rescue” like that of 2008 will be needed but may by then might have become impossible (Stockman 2013).[20] The alternative, the neoliberal reform cure which requires stripping society of its remaining defenses and throwing it into the icy waters of an untamed market economy, in the hope that it will eventually start swimming, may be rejected by the voting public as long as there still is one. The result may be a political stand-off like in Italy or France, which is not likely to encourage economic growth either.

What if a resumption of growth, as implied by older traditions of political economy, would require more public investment rather than less, and perhaps also a reversal of the apparently inexorable trend toward ever more inequality (Stiglitz 2012)? In this case, the declining capacity of politics to contain the plundering of the public sphere and the apparently unending self-enrichment of the already unendingly rich may pose a problem not just for democracy, but also for the economy – see the super rich among the Greeks who are abandoning Greece in droves, availing themselves of free international capital markets to take their money to the safe havens of Wall Street or the City of London; or the Russian and Ukrainian “oligarchs” who, having expropriated their fellow-citizens in post-communist primitive accumulation, are abandoning them to their domestic misery. What we are seeing here may be the beginning of the fate of economic elites becoming divorced from that of the economies-cum-societies from where they have derived their riches, decoupling the fortunes of the rich and their families from the prosperity, or the lack of it, of normal people.

Does this sound outlandish? Consider the current state of the distributional game in the United States, a country that, unlike Ukraine or China, is still considered a democracy. According to Emmanuel Saez, in 2010, the Year Two after the crisis, at a time of high unemployment and record public debt, 93 percent of all income gains in the U.S., i.e., almost the entire amount by which the national income increased, went to the top one percent of the income distribution. What is more, the top 0.01 percent, about 15,000 households, received more than a third, 37 percent, of those income gains (Saez 2012).[21] There is no reason not to call this an asset stripping operation of epic dimensions perpetrated by a tiny minority benefiting, among other things, from the deepest tax cuts in history. Why should the new oligarchs be interested in their countries’ future productive capacities and present democratic stability if, apparently, they can be rich without it, processing back and forth the synthetic money produced for them at no cost by a central bank for which the sky is the limit, at each stage diverting from it hefty fees and unprecedented salaries, bonuses and profits as long as it is forthcoming — and then leave their country to its remaining devices and withdraw to some privately owned island?

REFERENCES

Blyth, Mark, 2013: Austerity: The History of a Dangerous Idea. Oxford: Oxford University Press.

Boyer, Robert, 2012: The four fallacies of contemporary austerity policies: the lost Keynesian legacy. Cambridge Journal of Economics. Vol. 36, No. 1, 283-312.

Buchanan, James M., 1958: Public Principles of Public Debt: A Defense and Restatement. Homewood, Ill.: Richard R. Irwin, Inc.

Buchanan, James M. and Gordon Tullock, 1962: The Calculus of Consent: Logical Foundations of Constitutional Democracy. Ann Arbor: Univrsity of Michigan Press.

Buchanan, James M. and Gordon Tullock, 1977: The Expanding Public Sector: Wagner Squared. Public Choice. Vol. 31, 147-150.

Buchanan, James M. and Richard E. Wagner, 1977: Democracy in Deficit: The Political Legacy of Lord Keynes. New York: Academic Press.

Crouch, Colin, 2009: Privatised Keynesianism: An Unacknowledged Policy Regime. British Journal of Politics & International Relations. Vol. 11, No. 3 382-399.

Duménil, Gérard and Dominique Lévy, 2004: Capital Resurgent: Roots of the Neoliberal Revolution. Cambridge, Mass.: Harvard University Press.

Genschel, Philip and Peter Schwarz, 2013: Tax Competition and Fiscal Democracy. In: Schäfer, Armin and Wolfgang Streeck, eds., Politics in the Age of Austerity. Cambridge: Polity,

Greider, William, 1981: The Education of David Stockman. The Atlantic. No. December 1981.

Hacker, Jacob and Paul Pierson, 2011: Winner-Take-All Politics: How Washington Made the Rich Richer — and Turned Its Back on the Middle Class. New York City: Simon & Schuster Paperbacks.

Herndon, Thomas, Michael Ash and Robert Pollin, 2013: Does High Public Debt Consistently Stifle Economic Growth? A Critique of Reinhart and Rogoff. Political Economy Research Institute Working Paper Series No. 322. Amherst, Mass.: University of Massachusetts Amherst.

Judt, Tony, 2005: Postwar: A History of Europe Since 1945. London: Penguin.

Judt, Tony, 2009: What Is Living and What is Dead in Social Democracy? The New York Review of Books. No. December 17, 2009, 86-96.

Karabel, Jerome, 2012: Grand Illusion: Mobility, Inequality, and the American Dream, The Huffington Post.

Kenworthy, Lane, 2007: Egalitarian Capitalism: Jobs, Incomes, and Growth in Affluent Countries. New York, NY: Russell Sage.

Kochan, Thomas A., 2013: The American Jobs Crisis and Its Implications for the Future of Employment Policy: A Call for a New Jobs Compact. International Labor Relations Review. Vol. 66, No. 2, 291-314.

Korpi, Walter, 1983: The Democratic Class Struggle. London: Routledge and Kegan Paul.

Krippner, Greta R., 2011: Capitalizing on Crisis: The Political Origins of the Rise of Finance. Cambridge: Harvard University Press.

Kristal, Tali, 2010: Good Times, Bad Times: Postwar Labor’s Share American Sociological Review. Vol. 75, No. 5, 729-763.

Mehrtens, Philip, 2013: Staatsentschuldung und Staatstätigkeit: Zur Transformation der schwedischen politischen Ökonomie. Doctoral Dissertation. Köln: Universität Köln und Max-Planck-Institut für Gesellschaftsforschung.

Mertens, Daniel, 2013: Privatverschuldung in Deutschland: Zur institutionellen Entwicklung der Kreditmärkte in einem exportgetriebenen Wachstumsregime. Doctoral Dissertation. Köln: Wirtschafts- und Sozialwissenschaftliche Fakultät. Universität Köln und Max-Planck-Institut für Gesellschaftsforschung.

Merton, Robert K., 1968: The Matthew Effect in Science. Science. Vol. 159 No. 3810, 56-63.

Palley, Thomas I., 2008: Financialisation: What it is and Why it Matters. IMK Working Paper No. 4/2008. Düsseldorf: Institut für Markoökonomie und Konjunkturforschung.

Pierson, Paul, 1998: The Deficit and the Politics of Domestic Reform. In: Weir, Margaret, ed., The Social Divide: Political Parties and the Future of Activist Government. Washington, D.C., New York: Brookings Institution Press and Russell Sage Foundation, 126-178.

Pierson, Paul, 2001: From Expansion to Austerity: The New Politics of Taxing and Spending. In: Levin, Martin A. et al., eds., Seeking the Center: Politics and Policymaking at the New Century. Washington D.C.: Georgetown University Press, 54-80.

Reich, Robert B., 2007: Supercapitalism. New York: Alfred A. Knopf.

Reinhart, Carmen M. and Kenneth S. Rogoff, 2010: Growth in a Time of Debt. American Economic Review: Papers & Proceedings. Vol. 100 No. May 2010, 573-578.

Ross, A. M. and P. T. Hartman, 1960: Changing Patterns of Industrial Conflict. New York: Wiley.

Ruggie, John Gerard, 1982: International Regimes, Transactions and Change: Embedded Liberalism in the Postwar Economic Order. International Organization. Vol. 36, No. 2, 379-399.

Ryner, Magnus, 2012: The (I)PE of Falling Wage-Shares: Situating Working Class Agency. Prepared for Presentation at the Inaugural Conference of the Sheffield Political Economy Research Institute (SPERI) ‘The British Growth Crisis: The Search for a New Model’ Sheffield, UK, July 17, 2012. Unpublished Manuscript.

Saez, Emmanuel 2012: Striking it Richer: The Evolution of Top Incomes in the United States (Updated with 2009 and 2010 estimates).

Schäfer, Armin and Wolfgang Streeck, 2013: Introduction. In: Schäfer, Armin and Wolfgang Streeck, eds., Politics in the Age of Austerity. Cambridge: Polity.

Schratzenstaller, Margit, 2011: Vom Steuerwettbewerb zur Steuerkoordinierung in der EU? WSI-Mitteilungen. Vol. 64, No. 6, 304-313.

Schratzenstaller, Margit 2013: Für einen produktiven und solide finanzierten Staat. Determinanten der Entwicklung der Abgaben in Deutschland. Studie im Auftrag der Abteilung Wirtschafts- und Sozialpolitik der Friedrich-Ebert-Stiftung Bonn: Friedrich-Ebert-Stiftung

Schumpeter, Joseph A., 1991 [1918]: The Crisis of the Tax State. In: Swedberg, Richard, ed., The Economics and Sociology of Capitalism. Princeton: Princeton University Press, 99-141.

Shonfield, Andrew, 1965: Modern Capitalism: The Changing Balance of Public and Private Power. London and New York: Oxford University Press.

Shonfield, Andrew and Suzanna Shonfield, 1984: In Defense of the Mixed Economy. Oxford: Oxford University Press.

Stiglitz, Joseph E., 2012: The Price of Inequality: How Today’s Divided Society Endangers Our Future. New York: W. W. Norton.

Stockman, David A., 1986: The Triumph of Politics: How the Reagan Revolution Failed. New York: Harper and Row.

Stockman, David A., 2013: State-Wrecked: The Corruption of Capitalism in America. New York Times, March 31, 2013. Vol.

Streeck, Wolfgang, 2011: The Crises of Democratic Capitalism. New Left Review. Vol. 71, No. Sept/Oct 2011, 5-29.

Streeck, Wolfgang, 2013: Gekaufte Zeit: Die vertagte Krise des demokratischen Kapitalismus. Berlin: Suhrkamp.

Streeck, Wolfgang and Christine Trampusch, 2006: Economic Reform and the Political Economy of the German Welfare State. In: Dyson, Kenneth and Stephen Padgett, eds., The Politics of Economic Reform in Germany: Global, Rhineland or Hybrid Capitalism? Milton Park, Abingdon: Routledge, 60-81.

Thierry, B. , 2005: Integrating proximate and ultimate causation: Just one more go! Current Science. Vol. 89 No. 7, 1180-1184.

Tomaskovic-Devey, Donald and Ken-Hou Lin, 2011: Income Dynamics, Economic Rents and the Financialization of the US Economy. American Sociological Review. Vol. 76, No. 4, 538-559.

Western, Bruce and Jake Rosenfeld, 2011: Unions, Norms, and the Rise in U.S. Wage Inequality. American Sociological Review. Vol. 76, No. 4, 513-537.

NOTES

[1] For an elaboration see Streeck (2013, 164ff., passim). An alternative term would be austerity state.

[2] “The public finances are one of the best starting points for an investigation of society, especially but not exclusively of its political life. The full fruitfulness of this approach is seen particularly at those turning points, or epochs, during which existing forms begin to die off and to change into something new. This is true both of the causal significance of fiscal policy (insofar as fiscal events are important elements in the causation of all change) and of the symptomatic significance (insofar as everything that happens has its fiscal reflection).” (Schumpeter 1991 [1918], 110)

[3] For the purpose of this treatment I will consider declining growth as exogenous.

[4] This is essentially what Pierson (1998; 2001) refers to as an “austerity regime”.

[5] In other words, democratic capitalism implies a politics with a redistributive-egalitarian bent; indeed with reference to the postwar political formation in the West one could just as well speak of egalitarian capitalism (Kenworthy 2007). One implication is that not every political interference with market outcomes is “democratic” as the term is used here; for example, for the Bush tax cuts to be passed, democracy as we know it had to be anaesthetized rather than activated.

[6] Figure 3 does not include Sweden where union density was traditionally the highest in the world. Including it would have distorted the scale. Apart from this, the Swedish trajectory was very much in line with the other countries, except that the decline started later. At the beginning of the 1990s, union density in Sweden was still above 80 percent; by 2011, in about two decades, it had fallen to 68 percent.

[7] The average rate of unemployment in the OECD was 2.2 percent from 1960 to 1973, from where it increased steadily to 7.1 percent in 1990 to 2001. From 2002 to 2008 it was at 5.8 percent, only to rise to 6.6 percent between 2009 and 2012.

[8] Kochan refers to the historical watershed of the late 1970s as to the breaking of the postwar “social contract”(Kochan 2013).

[9] For Europe, see Schratzenstaller (2011).

[10] Redistribution to the poor had by this time already been privatized, i.e., relocated to deregulated financial markets where citizens were allowed to make up for stagnant incomes by taking up ever riskier loans (Crouch 2009). After 2008, these ended to a large extent on the public balance sheet.

[11] That tax cuts for the well-to-do cause public deficits, which are then used to argue the need for cuts in social welfare spending, is by no means limited to the United States. The same pattern was effective in Europe, including Germany ( Schratzenstaller 2013) where the losses in revenue caused by the Schröder tax reform were for several years the only reason why the federal government was unable to achieve a balanced budget. The deficit later became a central argument for the Hartz reform of the German welfare state.

[12] EXPLAIN: because it had encouraged an unsustainable leveraging of capitalist economies.

[13] The general picture remains the same if the debt of the financial sector is excluded.

[14] While there has been considerable excitement recently on a calculation error and the method of sample construction in Reinhart and Rogoff’s 2010 paper (Herndon et al. 2013), what should have caused consternation much earlier is their idea, mechanistic if nothing else, of a “one size fits all” general debt threshold for all countries, regardless of political and economic circumstances – not to mention that high debt may be the effect of low growth rather than vice versa.

[15] “Lloyd Blankfein, the head of giant investment bank Goldman Sachs, has said the UK must stick with its austerity plan or face a negative reaction from global investors. In an interview with the BBC, he said he would like it if the UK could ease the pace of the squeeze on spending. But Mr. Blankfein … said if you have a deficit that choice is taken away from you because markets will react.” BBC News, April 23, 2013

[16] Means of restoring creditor confidence may include a low general level of public spending, low taxes and a lean state, a de-unionized economy, all major political parties subscribing to fiscal rectitude and committed to a healthy financial industry, and the like.

[17] The U.S. is a special case, not only because of its role as global central banker of last resort. In U.S domestic politics, it seems firmly settled that the demands of creditors will always have priority over the rights of citizens, and that explicit debt will be served no matter what, even if implicit debt has to be given a “haircut” if necessary. This has not been as clear in Europe, at least not until a few years ago.

[18] “Within our mandate, the ECB is ready to do whatever it takes to preserve the euro. And believe me, it will be enough.” Verbatim of the remarks made by Mario Draghi, at the Global Investment Conference in London, 26 July 2012. Website of the European Central Bank, read April 27, 2013.

[19] EXPLAIN: today easy ECB money and ECB credit and purchasing programs cause convergence of risk premiums while at the same time salvaging banks, but this cannot last forever

[20] EXPLAIN: need to get off QE!

[21] As summarized by Steven Rattner in the New York Times, March 25, 2012: “In 2010, as the nation continued to recover from the recession, a dizzying 93 percent of the additional income created in the country that year, compared to 2009 — $288 billion — went to the top 1 percent of taxpayers, those with at least $352,000 in income. That delivered an average single-year pay increase of 11.6 percent to each of these households. Still more astonishing was the extent to which the super rich got rich faster than the merely rich. In 2010, 37 percent of these additional earnings went to just the top 0.01 percent, a teaspoon-size collection of about 15,000 households with average incomes of $23.8 million. These fortunate few saw their incomes rise by 21.5 percent. The bottom 99 percent received a microscopic $80 increase in pay per person in 2010, after adjusting for inflation. The top 1 percent, whose average income is $1,019,089, had an 11.6 percent increase in income.”

3 thoughts on “The Politics of Public Debt”